Phase 1 – Tell your story to create interest

Part 1 of 2 in a series looking at the Capital Raising struggle. Look out for part 2 – Extend Your Reach

In my research through pages and pages of a search engine, it revealed little or no information on the vast numbers of projects/funds looking at funding, compared to the numbers of projects/funds that succeed. What was apparent to me was the mind boggling numbers looking at funding and the limited few that were funded. The route to the funder is not only heavily congested but one full of failure, loss of time, money and effort. This article, writes Edward Simpson, looks at the importance therefore of your narrative to create interest in you.

If we take a moment to look at this from the funder’s perspective they are inundated with funds, project’s, entrepreneur’s and so forth all armed with let’s face it poorly written prospectuses, I have seen fintech funds going to market and they don’t even have a website. Funders in the case of a number of private equity managers I know now adopt AI, one such private equity manager received approx. 3000 prospectuses in a year, AI selected 3 that matched investment strategy, the human got involved and all 3 were declined. A funder on average invests in fewer than 0.3% in a given year those seeking investment would see this as low whereas the funder might see this as perhaps too high.

How then can we ensure your project/fund is noticed? What is the alternative, how does a project/fund generate interest in its route to funding? Filling up email inboxes leads to negative branding, connecting your story with interested funder’s who are searching right now for opportunity is what Finscoms does.

We have now identified the problem – list of applicants high, funder’s time is short.

Solution – an improvement/investment into communications to tell your story will generate interest.

I believe there to be a stunning lack of communication and communications skills in the route to the funder, this may well be the number one barrier achieving funding or at the least one of the major components to a lack of funding/interest?

“The most powerful person in the world is the storyteller. The storyteller sets the vision, values and agenda of an entire generation that is to come.” – Steve Jobs

What creates interest? Too many are overfamiliar with their project/fund, leaving the reader to ask ‘what is this about’. Easy to mention financials, the solution to the problem, is your story needs to encourage a funder to read further into your document not to give them reasons to say no.

Below is what a funder is looking for, this is based on feedback from the funder and differs from what the project/fund thinks the funder wants to see:

- Your team – Who are you and why are you suited/your expertise to lead this project/fund? Avoid the ‘I am an entrepreneur with loads of experience but no success’

- Product or Service – What exactly does your project/fund do exactly? Avoid a generic description and too much technical information. What specific results are/can be achieved? What is your solution to a problem?

- Market Demand – What is the potential for your project? What are your USPs? Why would anyone care about your project/fund? Avoid ‘everyone will need this’ or ‘its the next Google’

- Market Sector – Describe the market sector. Give examples of how your project/fund adds to its sector, is it sustainable? Does it have green credentials, show the value adds.

- Competition – Who else is in your sector, what is the competition – give examples. What are your differentiators?

- Financials – Include the amounts you are seeking for funding, what type of funding be it equity/debt/hybrid, what are your plans with the funding?

Effective communication means telling your audience a story funder’s understand, that captivates them and that makes them want to come back for the next chapter. Create hook’s with the above to create interest yes, but to also open up dialogue leading to a discovery call. Digital Marketing today allows for and creates inbound enquiries. Given recent lockdowns, funders are researching projects/funds, if the story is good they will make contact, you’ve now bypassed the high failure rate of projects/funds and their congested route to the funder.

Is it all about effective communications absolutely not, to tell your story in the first place you need a foundation a brand, create that all important first impression. A wise and small investment on your marketing materials, your projects/fund is well placed to tell the story, this small investment in your foundation is an asset that you own, shows a funder that you are understanding of the traditional and digital world’s with high returns on investment, telling your story is made all the easier to create.

If all this is too much, or you don’t have the time nor skills then Finscoms can help.

Whether you are just starting out or an established project/fund we can help. Why not send us your project/fund to mkt@finscoms.com we will reply with where we can help or not, improve the visuals, the telling of your story, to what audience, there is no cost to do this you have nothing to lose.

Finscoms are a full services marketing and communication’s company, we do not sell product nor do we give investment advice. With our expertise we do help you in your route to funding, we have a network of funder’s whom we could introduce you to.

Edward Simpson

Founder and Co Managing Partner

Connect with Edward on Linkedin

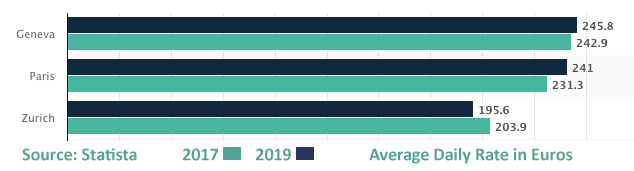

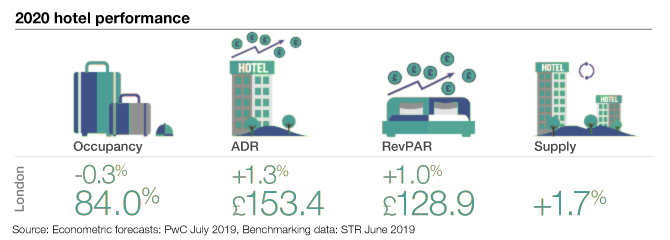

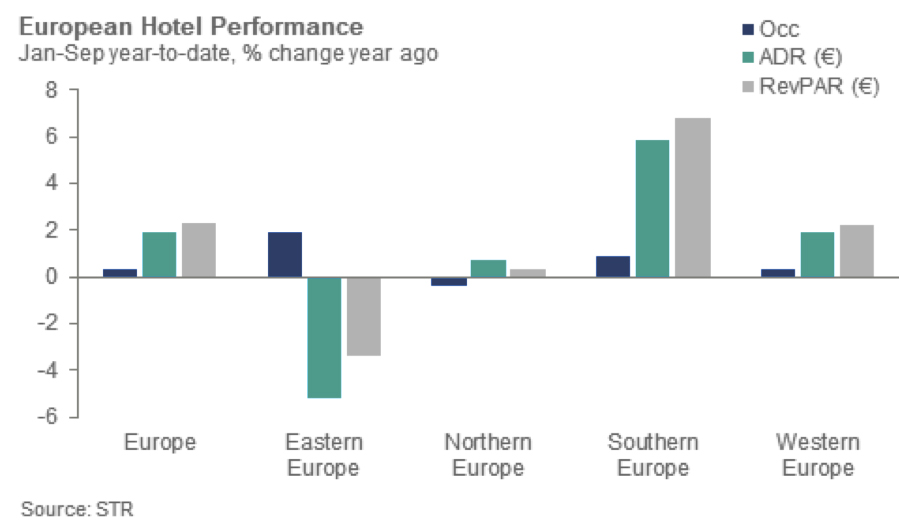

The European Travel Commission’s (ETC) latest quarterly report for Q3 2019 also states that European tourism demand remains in positive territory, notwithstanding a slower expansion rate compared to the previous two years. External risks remain for now but destinations continue to grow at a modest pace and the predominant regional outlook remains positive.

The European Travel Commission’s (ETC) latest quarterly report for Q3 2019 also states that European tourism demand remains in positive territory, notwithstanding a slower expansion rate compared to the previous two years. External risks remain for now but destinations continue to grow at a modest pace and the predominant regional outlook remains positive.